23 December 2024, Mon |

4:33 PM

23 December 2024, Mon |

4:33 PM

How to help the small business sector access the $5.2tn it needs to thrive.Across the world, micro, small and medium-sized enterprises (MSME) are vital engines of economic growth and job creation. According to the World Bank, MSMEs make up 90% of businesses and account for more than 50% of employment worldwide. In Dubai, MSMEs employ around 52% of the overall workforce and generate 50% of the Emirate’s GDP.

Going forward, it is estimated that around 600 million new jobs will be needed across the world between now and 2030 to absorb a rapidly growing workforce. In emerging markets, MSMEs create between 70 and 95% of all new jobs. Yet, despite their obvious importance to overall economic wellbeing, MSME failure rates can be as high as 50% within the first five years. The problem appears to be down to money and access to funding.

According to the International Finance Corporation, 65 million enterprises, in 128 developing countries across the globe have an unmet financing need of $5.2 trillion every year. This is a figure equivalent to 19% of the gross domestic product (GDP) of these countries.

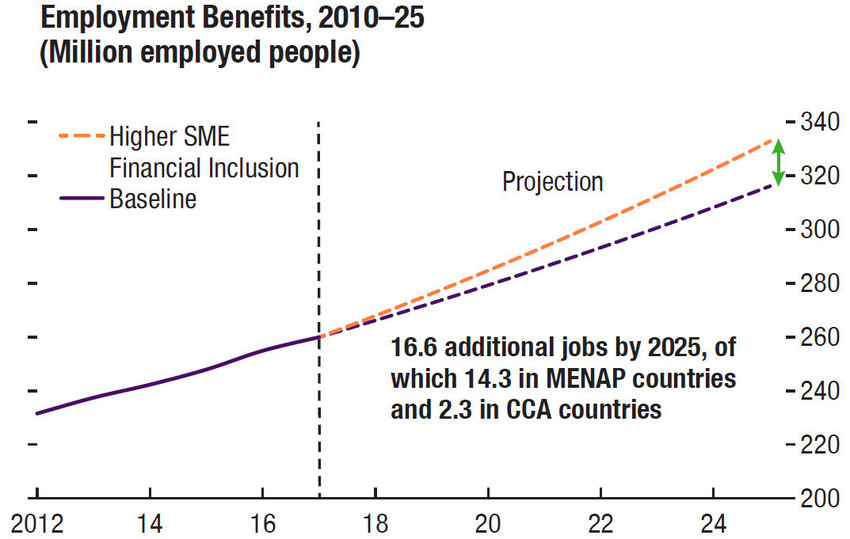

In the Middle East and Northern Africa (MENA) region, MSMEs represent about 96% of registered companies and about half of all employment, yet account for only 7% of total bank lending. Increasing the MSME bank lending rate to around a quarter could, according to the International Monetary Fund (IMF), create 15 million new jobs and boost MENA GDP by 1% annually by 2025.

How to help the small business sector access the $5.2tn it needs to thrive.

Across the world, micro, small and medium-sized enterprises (MSMEs) are vital engines of economic growth and job creation. According to the World Bank, MSMEs make up 90% of businesses and account for more than 50% of employment worldwide. In Dubai, MSMEs employ around 52% of the overall workforce and generate 50% of the Emirate’s GDP.

Going forward, it is estimated that around 600 million new jobs will be needed across the world between now and 2030 to absorb a rapidly growing workforce. In emerging markets, MSMEs create between 70 and 95% of all new jobs. Yet, despite their obvious importance to overall economic wellbeing, MSME failure rates can be as high as 50% within the first five years. The problem appears to be down to money and access to funding.

According to the International Finance Corporation, 65 million enterprises, in 128 developing countries across the globe have an unmet financing need of $5.2 trillion every year. This is a figure equivalent to 19% of the gross domestic product (GDP) of these countries.

In the Middle East and Northern Africa (MENA) region, MSMEs represent about 96% of registered companies and about half of all employment, yet account for only 7% of total bank lending. Increasing the MSME bank lending rate to around a quarter could, according to the International Monetary Fund (IMF), create 15 million new jobs and boost MENA GDP by 1% annually by 2025.

image via weforum

Accessing the levels of finance needed to survive and grow is perhaps the most fundamental challenge that MSMEs face. As many of these enterprises do business using only cash, building a credit history can be impossible, making it hard for traditional lenders to assess their creditworthiness. Without credit, financially excluded businesses become caught in cycles that restrict their capacity to grow and leave them underprepared for the effects of market disruption. Now is the time to redefine finance for good. This has never been more relevant than during the COVID-19 lockdown, where many businesses were forced to shut and relied on loans to survive.

Technology, particularly Open Banking, where customer data is shared securely between bank and non-bank partners, is among the tools that can play a major role in overcoming these challenges. It is therefore vital that governments, trade organizations, banks and technology providers come together to help MSMEs benefit from broader access to financial services. At Finastra, we are proud of the part that we as a fintech company are playing in this process.

To help bridge the SME funding gap in Kenya, Finastra is piloting a revolutionary microfinance initiative, Trust Machine. Developed with partners in data, financial literacy, blockchain and scenario modelling, the resulting loan and balance sheet optimization solution aims to reduce the country’s $19bn business funding gap by 1%, a development that could create up to 50,000 new jobs and support sustainable economic growth.

The move to cloud has been particularly crucial during lockdown, with bank branches around the world being forced to close. We’ve witnessed an acceleration in digital transformation strategies as institutions look to better understand their financial positions, particularly in their capacity to connect with their customers during these critical times. Recently, Finastra worked with CIH Bank, a Morocco-based commercial bank, to complete an accelerated implementation of Fusion Corporate Channels. As a result, corporate customers of CIH Bank were able to move to fully digitalized trade finance operations, a transition that meant those companies could continue to operate seamlessly during the recent COVID-19 lockdown period.

The increasing availability of affordable software as a service (SaaS) platforms is making it easier for MSMEs to digitize their accounts, which is another reason to be optimistic about their prospects. This will enable them to create a trail of records, making it easier for lenders to assess a company’s viability and long-term potential.

The rewards of rapid evolution, and the subsequent affordability of digital payment solutions, are being reaped by merchants. This is of pertinence with the adoption of data interchange standards such as ISO 20022. Under the Vision 2030 strategy, for example, Saudi Arabia aims for 70% of all payments to be electronic in 2030, up from 18% in 2016 and 28% in 2020. Being able to process card payments affordably will greatly increase MSMEs’ addressable customer base.

There is good reason to believe that MSMEs will soon find it easier to access the capital needed to avoid grinding to a halt. The speed at which we emerge from the economic slowdown caused by COVID-19 may depend on it.