25 November 2024, Mon |

11:28 AM

By: Tonya Chin, SVP Corporate Marketing and IR, and Chief Communications Officer at Nutanix

The hyper-converged infrastructure (HCI) market has been on a fast journey over the past few years. Starting as a hardware-centric market focused on the simplicity of procuring datacenter hardware and software in one fell swoop, it quickly shifted as software-centric technology vendors and customers alike realized the biggest value一and innovation一was in the software. This is probably not surprising to those closely following the HCI market now but then it was a big change in the IT industry, as it evolved to embrace software-defined offerings.

This shift also came with challenges, particularly that of evaluating market share. At the beginning of 2020, I shared my thoughts on the effectiveness of IDC’s Converged Infrastructure Tracker, calling for a reevaluation of their methodology to separately focus on software sales, without accounting for hardware. We knew these numbers would tell a very different story, and were eager to share this with the market at large.

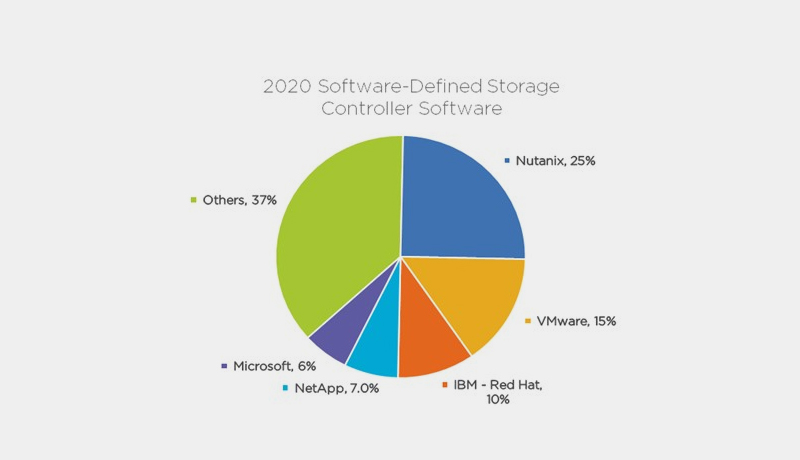

I’m ecstatic to share that IDC just released their Software-Defined Storage Controller Software Market Share, which encompasses the HCI software market along with software for block, file, and object offerings. Here, as I have long asserted, Nutanix is clearly the market leader with 25% of the market, well ahead of the nearest competitor at 15%.

This has been the result of extensive work from IDC to completely reevaluate a quickly evolving market. One that required rethinking the status quo to keep up with the pace of technology innovation and sales. We’re deeply grateful to IDC for realizing that there was a gaping hole in the market when it came to HCI software, and bringing this project to completion while giving Nutanix the credit that we long knew it was due.

According to IDC, the Software-Defined Storage Controller Software market is part of a new market share report by IDC focused on Software-Defined Infrastructure (SDI). From IDC:

“SDI refers to logically pooled resources of compute, memory, storage, and networking, which are managed by software with minimal human intervention. SDI systems are independent of the underlying hardware, as long as the hardware meets certain technical specifications. The underlying hardware in SDI systems are industry-standard, commercial off-the-shelf (COTS) products that have enterprise-grade certifications.”

IDC divides the SDI market in three areas: software-defined compute software, software-defined networking software, and software-defined storage controller software (SDSCS). The last one, SDSCS, includes and combines block, file, object, and hyperconverged software offerings that enable the creation of a storage system.

Here, IDC shares:

“SDS-CS is the core software that virtualizes and pools the storage resources across different servers that comprise the SDS. SDS-CS provides for data persistence, a set of data services (snapshots, replication, etc.), and a method of data organization (block, file, and/or object) along with one or more defined access methods (block, file, and/or object). Another way to describe an SDS system is that it has modular building blocks, uses industry-standard hardware platforms, and typically employs distributed, scale-out architecture.”

While this is a broader view than just HCI, HCI software represents the vast majority of the market included in this new view. This is also the cleanest view of the HCI software market. The only public one that allows the industry to compare the largest HCI software vendors without estimated hardware sales impacting, and in fact determining, market leadership calculations. Additionally, while IDC will continue to publish the Converted Tracker, they will no longer actively promote it within a formal press release, and shift their focus to this view instead. One that we believe is a more meaningful view into the HCI market as it continues to evolve.

For now, I want to thank IDC for all their work, and share a heartfelt congratulations to the Nutanix team, our customers and partners for all the hard work that led to this significant recognition!

Note: IDC 2H2020 Semiannual Software-Defined Infrastructure Tracker, June 2021. Market referenced is the calendar year 2020 software-defined controller software (SDS-CS) functional market. SDS-CS market includes all discrete file, block and object-based SDS-CS solutions as well as all hyperconverged SDS-CS solutions. Market is software only and excludes the value of hardware.